When the storm is coming, wouldn't it be better to have a local agent with catastrophic storm experience than a 1800 call center number?

ISU Bauknight Insurance operates two Counties in Florida, Hudson, FL (727) 863-5641 and ISU Bauknight Insurance, 10488 Spring Hill Drive, Spring Hill, Fl 34607 (352)-686-0612. They also offer coverage throughout Florida on their website or by calling them direct.

http://www.cnn.com/2017/08/25/us/hurricane-harvey/index.html

Subscribe To

Friday, August 25, 2017

Friday, July 14, 2017

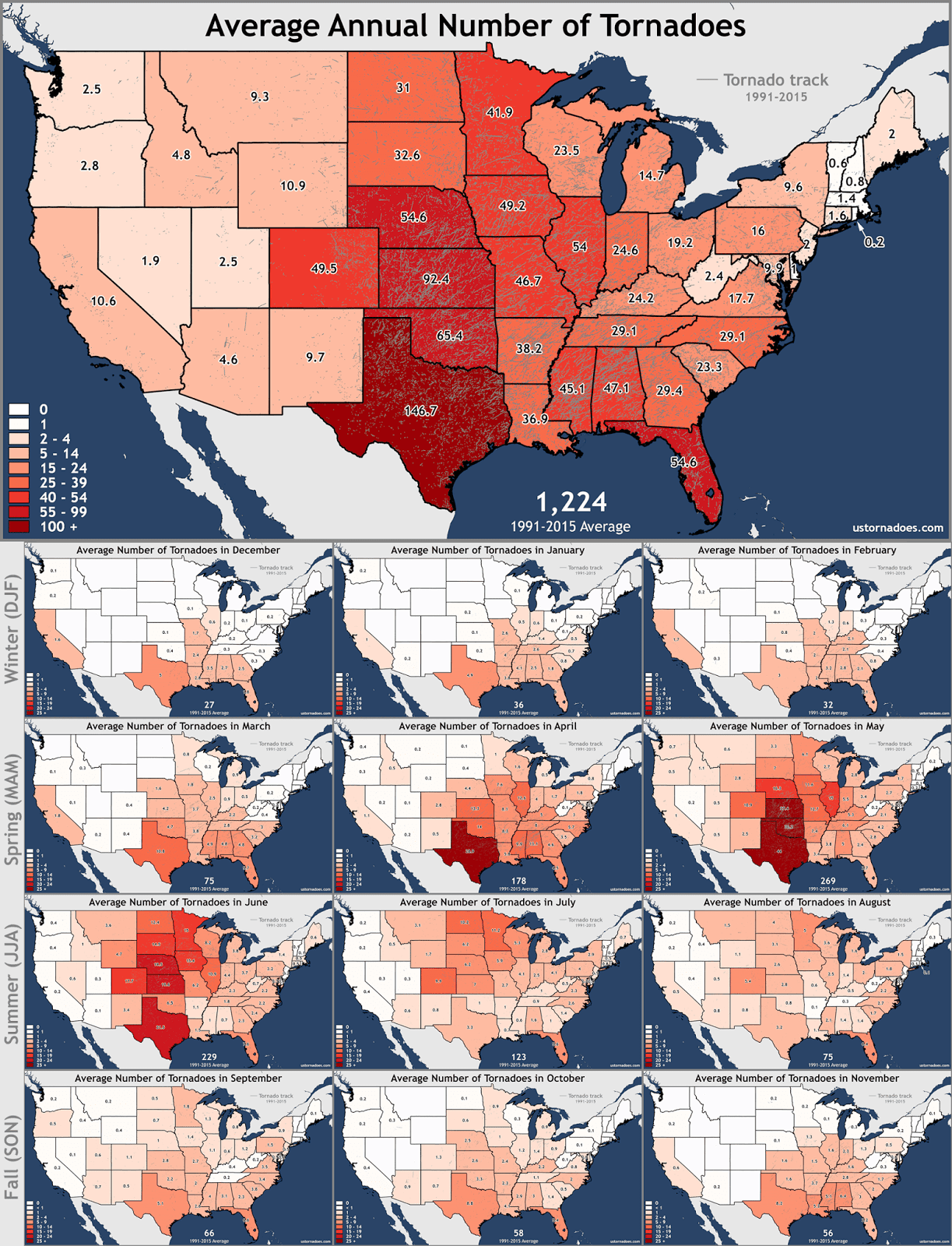

Tornado season

Real News Real Fast, our local internet news source, posted these pictures the other day of a tornado over Spring Hill, Fl.

Spring Hill is where our office is located. Tornado activity occurs frequently in Florida. In fact, Florida is ranked 4th in all the states for tornado formation, surprisingly beating out Nebraska, Iowa, and Missouri. The only states with more Tornado activity than Florida are Texas, Kansas and Oklahoma.

Even more surprisingly, In August and September, Florida generates tornadoes at the highest rate of ANY state in the nation.

Source:

Is your property properly covered for replacement cost? Does your policy cover damage by tornado? What is your deductible?

Let us review your coverage for you by calling us at 352-686-0612.

ISU Bauknight Insurance operates two Counties in Florida, Hudson, FL (727) 863-5641 and ISU Bauknight Insurance, 10488 Spring Hill Drive, Spring Hill, Fl 34607 (352)-686-0612. They also offer coverage throughout Florida on their website or by calling them direct.

Thursday, June 1, 2017

Hurricane season

Hurricane season officially starts today, June 1, 2017

Florida has been relatively lucky over the past ten years in spite of Hurricane Hermine and Hurricane Matthew. In 2016 these two storms caused Floridians to file 130,000 claims totaling almost 800 million dollars.

This year experts are predicting an active season with 11-14 named storms and 4-7 actual hurricanes with two of these storms being category 3 or higher.

All Floridians should be emergency prepared for hurricane season, including stockpiling bottled water, batteries. In addition its important to be properly insured and financially ready to pay deductibles on your policy.

the state of Florida has a financial preparedness tookit to help consumers check their readiness. you can find it here...

ISU Bauknight Insurance operates two Counties in Florida, Hudson, FL (727) 863-5641 and ISU Bauknight Insurance, 10488 Spring Hill Drive, Spring Hill, Fl 34607 (352)-686-0612. They also offer coverage throughout Florida on their website or by calling them direct.

Tuesday, March 14, 2017

The hartford named one of the Most ethical companies in the world

Hartford Insurance Company named as one of the world's most ethical companies.

Every year the Ethisphere Institute compiles a list of companies that operate in a manner that operate with high ethics and good business practices. This is their statement for 2017

"The Ethisphere Institute, a global leader in defining and advancing the standards of ethical business practices, today announced 124 companies spanning five continents, 19 countries and 52 industry sectors as the 2017 World’s Most Ethical Companies® honorees.

Since 2007, Ethisphere has honored those companies who recognize their role in society to influence and drive positive change in the business community and societies around the world. These companies also consider the impact of their actions on their employees, investors, customers and other key stakeholders and leverage values and a culture of integrity as the underpinnings to the decisions they make each day."

the companies selected are not affiliated with Ethisphere and are selected based on the following criteria:

"At the heart of the evaluation and selection process for Ethisphere’s World’s Most Ethical Companies is Ethisphere’s proprietary rating system, the corporate Ethics Quotient (EQ). The framework of the EQ is comprised of a series of multiple-choice questions that capture a company’s performance in an objective, consistent and standardized way. The information collected is not intended to cover all aspects of corporate governance, risk, sustainability, social responsibility, compliance or ethics, but rather is a comprehensive sampling of definitive criteria of core competencies. The EQ framework and methodology was determined, vetted and refined by the expert advice and insights gleaned from Ethisphere’s network of thought leaders and from the World’s Most Ethical Companies Methodology Advisory Panel."

Once again one of our partner companies, The Hartford, won the award for the 9th Time. we are proud to be associated with a company with such high standards!

For the complete list, see this link:

ISU Bauknight Insurance operates two Counties in Florida, Hudson, FL (727) 863-5641 and ISU Bauknight Insurance, 10488 Spring Hill Drive, Spring Hill, Fl 34607 (352)-686-0612. They also offer coverage throughout Florida on their website or by calling them direct.

Tuesday, February 28, 2017

Auto accidents increasing in Florida due to distracted drivers...

and by association, so are auto insurance rates.

Distracted driving has always caused accidents. In the past, reaching for the radio, lighting cigarettes, looking away during conversations, all these things caused people to take their attention off the road where it belonged.

With the advent of cell phones and especially smart phones, things have changed dramatically. Now it is the norm for people to text, watch videos, and fiddle with their phones during driving. One major auto insurance company (state farm) claims that 36% of drivers text and drive.

How serious is the problem? According to the National Highway Traffic Safety Administration, 40,000 american dies last year in auto accident, and distracted driving caused 9% of these deaths. This resulted in 3600 deaths due to distracted drivers. What the total cost in property and injuries is unknown.

What is known is that auto insurance premiums have increased Nationwide auto insurance has gone up 16% since 2011, and in Florida we have seen much more dramatic increases.

Auto Insurance rates reflect many things including the cost of repairs, the cost of medical care, auto theft rate, and the frequency and severity of accidents. Of these factors, we can all affect the last one. Put the phone down and text the person on the line when you stop the car. It may save your life or the life of someone your love.

ISU Bauknight Insurance operates two Counties in Florida, Hudson, FL (727) 863-5641 and ISU Bauknight Insurance, 10488 Spring Hill Drive, Spring Hill, Fl 34607 (352)-686-0612. They also offer coverage throughout Florida on their website or by calling them direct.

Wednesday, February 15, 2017

Demotech suspends their Florida Insurance rating model and warns that 10 -15 of their 57 rated property insurance carriers writing in Florida will be downgraded.

Okay, what does this mean, and who the heck is Demotech?

To understand who Demotech is and why this is significant, one needs to understand what it means to have an A rated Insurance company.

Before the Florida property Insurance crises, companies were typically rated 'A', 'B', 'C', or not issued a rating by a company called AM Best, a company with the purpose is to review insurance carriers and offer an independent review of their finances and operations as it relates to their ability to meet their obligations. If your carrier was not A rated, it was generally unacceptable by Mortgage companies.

After Hurricaine Andrew, most companies left Florida. Those remaining were not "A" rated by AM best, including major companies subsidiaries like State Farm and Allstate who had formed subsidiaries for Florida only.

Demotech is an alternative rating company that came in and in some opinons, gave A ratings to companies that did not earn it. In fact, some Florida companies with demotech A ratings have gone bankrupt. However the mortgage companies generally accepted this rating because, well, these were typically the only companies writing property insurance in Florida and of course they did want to sell mortgages to Florida homeowners. it remains a touchy situation.

Fast forward to 2016 which had volatile weather and has caused Demotech to have concern for some of the 57 carriers they rate. in addition, major court cases unfriendly to insurance companies has caused Demotech to rethink their rating model:

"Recent Florida Supreme Court decisions and ongoing abuse in Florida’s insurance market have led Demotech to change the criteria it uses when rating insurers in the state. The announcement comes as insurers get ready to announce their 2016 annual reports that could indicate unfavorable results for many.....[2016 catastrophes] eroded their surplus and after that had been eroded there was the Johnson and Sebo cases,” he said. “No one is in danger of going under, but that being said we have standards that are higher than just not going under.”

So what does this mean? It means that some property (homeowner) companies are not as financially healthy coming into 2017 as they were in 2016, and Demotech will be publishing a list of these companies they will downgrade.

We will publish that list here when it comes available. While we as an agency have no faith in Demotech's ability to predict financial stability, we do take notice when they downgrade a company. It's as if the teacher in school gives out almost all A grades, but gives one kid a C, it causes one to wonder just how bad the kid with a C performs.

If your company shows up on this list, you may run into issues with your bank accepting it. We are in a position to help you here, because we represent many homeowner Markets. Call us at 352-686-0612 if you find yourself in this situation.

ISU Bauknight Insurance operates two Counties in Florida, Hudson, FL (727) 863-5641 and ISU Bauknight Insurance, 10488 Spring Hill Drive, Spring Hill, Fl 34607 (352)-686-0612. They also offer coverage throughout Florida on their website or by calling them direct.

Monday, October 31, 2016

Subscribe to:

Posts (Atom)